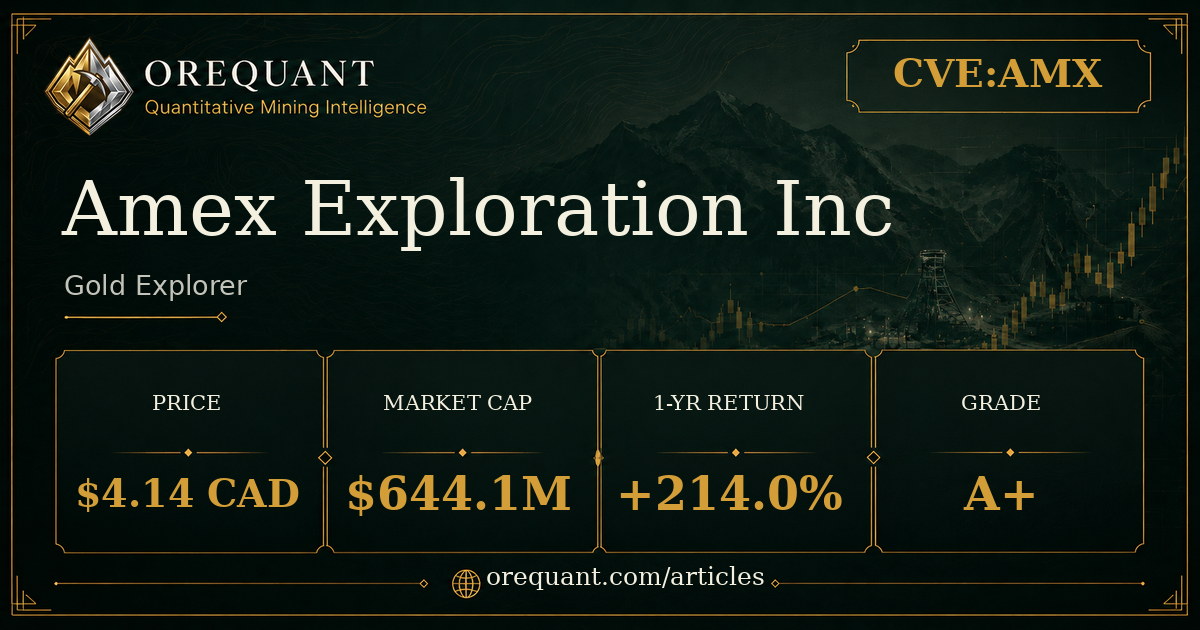

Amex Exploration Inc (AMX) July 2026 Snapshot: A+-Grade Gold Explorer

| Share price | $4.14 CAD |

|---|---|

| Market cap | $644.1M |

| 1-year return | +214.0% |

| 1-month return | -9.0% |

| OreQuant quality grade | A+ |

| Classification | explorer |

See the full signal depth behind this snapshot →

Snapshot

Amex Exploration Inc (CVE:AMX) is a junior gold explorer operating exclusively in Canada. It carries an A+ quality grade — the top band in OreQuant's relative rating system — placing it above its supplied peer group on current public-data scoring. The stock trades at C$4.14 with approximately 155.6 million shares outstanding, giving a market capitalization of roughly $644 million USD.

Recent price performance tells a sharply bifurcated story. Over the trailing month, AMX declined 9.02%. Over the trailing year, the stock gained 214% — a standout return within the junior gold explorer universe.

Amex Exploration fits the explorer archetype precisely: a pre-production company focused on exploration and resource definition that may require external capital to advance its projects. Revenue for the trailing period ending March 31, 2026 stands at zero, with the net loss reflecting capital consumed without any offsetting production income. That burn rate sets the financial context for everything that follows.

The explorer archetype, by definition, means the company's value proposition rests almost entirely on what lies beneath the ground — resource definition progress and the geological optionality embedded in its land holdings. Without a production decision or construction timeline, the market is pricing expected future resource value and the quality of the exploration pipeline, not any current cash-generating operation.

What They're Exploring

Amex Exploration holds five projects, all located in Quebec, Canada. The portfolio is concentrated within a single province across a single continent — North America. Quebec is a well-established mining jurisdiction with mature regulatory frameworks, reliable infrastructure access, and a long track record of supporting junior mining companies through the full exploration cycle. AMX's entire land package sits within it, which removes cross-border jurisdictional risk from the equation entirely.

The other four properties broaden the company's footprint within the province and provide geological diversification within a single jurisdiction. The primary commodity across all projects is gold.

Single-jurisdiction concentration carries a dual character.

With no mine construction underway and no stated production target across any of the five properties, Amex remains firmly in the exploration and resource-definition phase. This is fully consistent with its explorer classification and with the company's archetype definition as a pre-production entity that may require external capital to advance projects.

Among the supplied peer group, comparable names include Banyan Gold Corp (CVE:BYN), Meridian Mining UK Societas (TSE:MNO), Freegold Ventures Ltd (TSE:FVL), Larvotto Resources Ltd (ASX:LRV), and Troilus Mining (TSE:TLG). Quality grades across this cohort run C, B, B, D, and D respectively — placing AMX at the top of the group by OreQuant's relative grading.

OreQuant scores every company across 11 signal layers, updated daily. Start Your 7-Day Free Trial to see the full breakdown behind this snapshot.

Cash Position

Amex Exploration carries an active financing risk flag within the one-year window. For a zero-revenue explorer, this is a material operational consideration that shapes how the company can prosecute its exploration agenda. Trailing revenue through March 31, 2026 is precisely $0 — every dollar funding exploration, drilling, and administration must come from external capital markets, whether through equity issuance, private placements, or other financing mechanisms.

The net loss cited in the Snapshot section establishes a minimum cash consumption baseline, though total demands can vary with drill program intensity, the number of active project fronts, and any corporate activity that requires incremental spending. With five projects across Quebec, the company has multiple potential areas demanding capital allocation decisions simultaneously. Prioritization between the Perron Property flagship and the four secondary projects becomes a direct function of available treasury.

Amex has a sizeable equity base relative to many junior explorers, which in principle supports access to equity financing. A larger float and higher absolute market capitalization can make institutional participation in placements more feasible. However, the active financing risk flag confirms that near-term capital requirements remain an open and actively monitored consideration — the size of the equity base does not eliminate the risk, it merely conditions the terms on which capital might be accessed.

Junior explorers with a financing risk flag face a particular dynamic: their ability to advance projects depends on equity market receptivity, which is itself sensitive to gold price direction and broader risk appetite. A sustained decline in gold prices or a risk-off shift in equity markets can compress the ability to raise capital on acceptable terms. Conversely, a constructive gold price environment — as has broadly characterized the trailing twelve months — tends to support the financing window for well-regarded explorers. That said, the financing flag remains active regardless of trailing performance, and the near-term window warrants monitoring.

OreQuant's Read

AMX's A+ quality grade stands out within its supplied peer group, where grades run from B down to D. Per OreQuant's grading framework, this rating band is a relative assessment based on current public-data scoring — it does not independently establish management quality, financing capacity, or operational maturity. As a relative signal, the top-band grade is a meaningful differentiator across a cohort of similarly-sized junior gold explorers operating in broadly comparable market conditions.

The one-year performance comparison across the peer group illustrates the dispersion that characterizes junior explorers even within a tightly defined market-cap cohort. Meridian Mining returned 110% over the same period, Troilus Mining returned 178%, and Freegold Ventures declined 10.74% — a full reversal. Larvotto Resources registered no meaningful one-year change. The spread between the best-performing peer and the worst exceeds 490 percentage points, underscoring how differentiated outcomes are for junior gold explorers even when they share similar market capitalizations and commodity focus. Within that distribution, AMX's trailing return places it in the upper tier of the group.

Insider activity in the period reviewed did not show a concentrated cluster of recent transactions — a neutral read, neither confirming nor contradicting the grade signal. The active financing risk flag remains the most concrete near-term variable to monitor across all the public data supplied for this company. For a pre-production explorer with no revenue and five active project properties, the trajectory of the financing window is a primary operational constraint.

The picture for AMX is specific: a top-rated junior gold explorer in a well-established Canadian jurisdiction, carrying a strong one-year return, but with an active financing risk flag and no stated production target. The stock's performance has tracked gold's broader strength, amplified by the company's pre-production leverage to the metal. Investors following the gold explorer space will recognize AMX as a name that sits at the intersection of strong relative quality scoring and the structural capital dependency that defines the explorer category. The methodology underlying the grade accounts for that context rather than treating the quality band as a standalone endorsement.

Sector peer comparison

| Company | Ticker | Market cap | 1-yr return | Grade |

|---|---|---|---|---|

| Banyan Gold Corp | BYN | $641.8M | +483.0% | C |

| Larvotto Resources Ltd | LRV | $654.4M | — | D |

| Meridian Mining UK Societas | MNO | $633.6M | +110.0% | B |

| Freegold Ventures Ltd | FVL | $606.6M | -10.7% | B |

| Troilus Mining | TLG | $689.9M | +178.0% | D |

Peers ranked by market-cap proximity within the same commodity and producer tier. Market data and quality grades are public; OreQuant's full signal-layer scores are subscriber-only.

Frequently Asked Questions

What projects does Amex Exploration currently hold?

Amex Exploration holds five projects, all located in Quebec, Canada: the Perron Property, Cameron, Eastmain River, Abbotsford Project, and Hepburn Project. Gold is the primary commodity across all five.

How does AMX's quality grade compare to its peers?

AMX carries an A+ quality grade, the top band in OreQuant's relative rating system. Its supplied peer group — Banyan Gold (C), Meridian Mining (B), Freegold Ventures (B), Larvotto Resources (D), and Troilus Mining (D) — sits below AMX across the board. The grade is a relative assessment based on current public-data scoring and does not independently establish management quality or operational maturity.

Does Amex Exploration carry a financing risk flag?

Yes. Amex Exploration carries an active financing risk flag within the one-year window. The company generates zero revenue and is fully dependent on external capital markets to fund ongoing exploration activity.

What has AMX's recent price performance looked like?

Over the trailing year, AMX gained 214%. Over the trailing month, the stock declined 9.02%. Junior gold explorers with high leverage to the gold price frequently exhibit this kind of short-term volatility following large run-ups.

Is Amex Exploration in production?

No. Amex Exploration is classified as an explorer — a pre-production company focused on exploration and resource definition. There is no stated production target or mine construction underway across any of its five Quebec projects.

Risk & Disclosure

Gold mining equities carry substantial risk including commodity-price volatility, operational disruptions, jurisdictional changes, and capital allocation missteps. Senior producers mitigate some risks through diversification and scale, but remain sensitive to metal prices, cost inflation, and geopolitical developments. Junior and exploration-stage companies carry additional risk including total loss of capital. Past performance does not predict future results.

Investors should be prepared for double-digit intraday swings and should conduct independent due diligence, assess risk tolerance, and consult a licensed financial professional before initiating or modifying positions in mining equities.

OreQuant is not a registered investment advisor. This content is for informational and educational purposes only. It is not investment advice. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Mining equities — especially juniors — carry substantial risk including total loss of capital.

Subscribers access the full signal depth behind this snapshot — individual scores, insider cluster details, Monte Carlo valuation, and position sizing updated daily. Start Your 7-Day Free Trial.