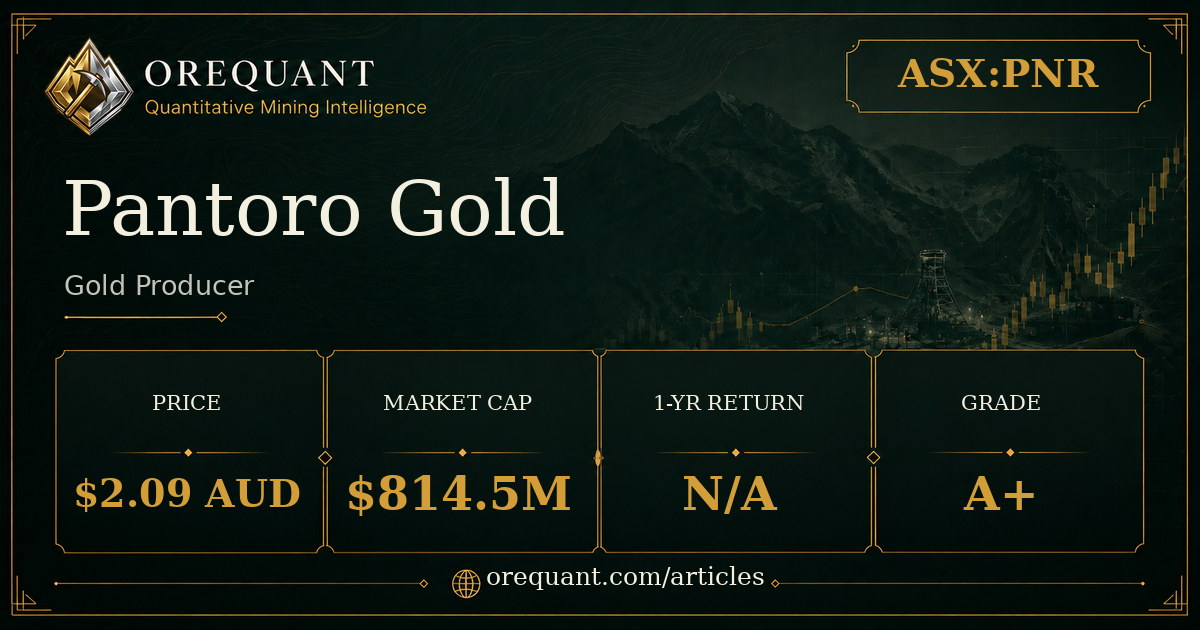

Pantoro Gold (PNR) July 2026 Snapshot: A+-Grade Gold Producer

| Share price | $2.09 AUD |

|---|---|

| Market cap | $814.5M |

| 1-month return | -13.5% |

| OreQuant quality grade | A+ |

| Classification | producer |

See the full signal depth behind this snapshot →

At a Glance

Pantoro Gold (ASX:PNR) is an operating gold producer with Australian assets, a market capitalization of approximately $815 million USD, and trailing twelve-month revenue of roughly $488 million USD recorded through FY2025. The company carries an A+ quality grade, as defined under OreQuant's grading framework.

Pantoro's share price is denominated in Australian dollars, consistent with its ASX listing. At a reported price of AUD 2.09 per share across approximately 390 million shares outstanding, the market capitalization reflects a company firmly within the producing cohort. The AUD denomination is relevant context: USD-translated figures carry an embedded currency effect whenever the Australian dollar moves against the greenback, and comparisons to non-Australian peers should account for that translation layer.

The one-month price return of -13.48% is the most notable short-term data point in the current snapshot. Net income of approximately $53 million USD against the TTM revenue figure confirms that production is translating, at least partially, to bottom-line results — a distinction worth preserving when comparing Pantoro to earlier-stage, pre-earnings peers in its sector cohort.

The A+ quality grade sits at the top of OreQuant's rating bands. As noted in the grade definition, the rating reflects a relative scoring outcome grounded in current public data; it does not independently establish management quality, financing capacity, or balance-sheet strength. Within the context of a producing gold company generating meaningful revenue, the grade frames PNR as occupying the upper tier of scored names in the system at the time of this snapshot.

What This Company Mines

Gold is Pantoro's sole reported commodity, and all operations are located within Australia — a single-continent footprint entirely within Oceania. The producer archetype, as defined in the system, describes an operating mining company with production-stage assets. The FY2025 financials confirm that definition in practice: Pantoro is generating revenue from gold extraction, not from capital market activity or resource delineation programs.

The Nicolsons Gold Mine and the Norseman Gold Project are both sited in Western Australia. The Halls Creek project and an additional Norseman listing also fall within Australian jurisdiction. This geographic concentration in Western Australia places Pantoro within one of the world's more established gold-mining regulatory environments, one with a long track record of permitting, infrastructure, and workforce availability for operating producers.

The multi-project structure within a single country has practical implications for operational diversification. At the same time, full exposure to a single jurisdiction means that regulatory, environmental, or macroeconomic changes affecting Australian mining would apply across the entire portfolio simultaneously.

Unlike explorers or developers, a producer generates operating cash flow from active mines rather than from capital raises or resource delineation work. Pantoro's TTM revenue confirms production-stage status unambiguously: the company is selling gold, not projecting future production from a hypothetical mine plan.

ASX announcements show multiple buy-back notifications filed across late June 2026, followed by a cessation of securities notification in early July 2026. For a gold producer at Pantoro's scale, an on-market buy-back is a capital allocation data point worth noting alongside the operational figures. A buy-back program, when run concurrently with confirmed earnings, indicates that the company was directing capital toward share reduction during that specific window — a factual observation about the use of corporate funds, not a directional signal about future price behavior.

OreQuant scores every company across 11 signal layers, updated daily. Start Your 7-Day Free Trial to see the full breakdown behind this snapshot.

How It Compares to Peers

OreQuant's system-defined peer set for PNR includes five companies: Thesis Gold & Silver (CVE:TAU), Liberty Gold (TSE:LGD), Gold Reserve Inc (CVE:GRZ), Wia Gold Ltd (ASX:WIA), and Javelin Minerals Ltd (ASX:JAV).

PNR and Gold Reserve Inc (CVE:GRZ) are the only two companies in the peer group rated A+. The remaining peers carry grades of D (Thesis Gold & Silver), C (Liberty Gold and Wia Gold), and F (Javelin Minerals).

One-year price performance diverges sharply across the group. Liberty Gold posted a one-year return of 374%; Thesis Gold & Silver returned 182%; Gold Reserve Inc returned 150%. The ASX-listed peers in this cohort have not participated in the price momentum visible among the Canadian-listed names. The divergence between the Canadian and Australian names is consistent across both ASX-listed peers in the group, suggesting a possible exchange-level or regional demand dynamic rather than a company-specific factor for PNR alone.

The peer comparison does not resolve the cause of PNR's relative lag against the Canadian names. Those companies carry lower quality grades — D, C, and A+ respectively — indicating meaningfully different underlying scoring profiles, which limits the utility of a direct return comparison as a standalone signal. Higher one-year price appreciation in lower-graded peers does not, by itself, imply that PNR's flat return reflects underperformance attributable to its fundamentals. Market re-rating dynamics in junior and mid-tier gold names often track sentiment and momentum as much as they track operational quality over any twelve-month window.

Wia Gold carries a C grade versus PNR's A+, and Wia's market capitalization of roughly $911 million is modestly above PNR's.

Why It Matters Now

Whether that reflects sector rotation, gold price movement, or company-specific selling pressure is not established by available data, but the magnitude and compression of the move into a single month warrants careful monitoring.

The buy-back notifications filed across late June 2026 and the subsequent cessation of securities notification in early July represent documented corporate activity running concurrently with the price decline. These are factual data points from ASX announcements. Multiple buy-back update filings within a compressed window suggest the program was active and ongoing during that period. A cessation of securities notification following the buy-back updates is a separate, distinct corporate event; neither filing alone explains the price behavior, and no causal relationship between the buy-back activity and the share price decline is supported by the data available here.

On the income side, net income and TTM revenue — both cited in the At a Glance section — indicate a positive but relatively thin margin against the revenue base. Margin compression or expansion in subsequent periods would require updated financial data to assess.

The combination of confirmed profitability, a multi-project Western Australian gold portfolio, an active capital return program documented in ASX filings, and a top-band quality grade positions PNR as a name with several observable data points aligning simultaneously. The sharp one-month price decline introduces a gap between the fundamental and price-based signals that the current snapshot captures but does not resolve.

Taken together, the top-band quality grade, confirmed production-stage status, and active capital return activity frame PNR as a monitoring candidate at a moment when its share price has pulled back sharply from levels seen across the prior portion of the trailing period. The current price level represents a material move from where the stock traded over the prior eleven months of the same trailing window, and the flat annual return obscures the intra-period volatility that the one-month figure makes visible.

Sector peer comparison

| Company | Ticker | Market cap | 1-yr return | Grade |

|---|---|---|---|---|

| Thesis Gold & Silver | TAU | $800.6M | +182.0% | D |

| Liberty Gold | LGD | $790.3M | +374.0% | C |

| Gold Reserve Inc | GRZ | $789.2M | +150.0% | A+ |

| Wia Gold Ltd | WIA | $910.5M | — | C |

| Javelin Minerals Ltd | JAV | $716.9M | — | F |

Peers ranked by market-cap proximity within the same commodity and producer tier. Market data and quality grades are public; OreQuant's full signal-layer scores are subscriber-only.

Frequently Asked Questions

What commodity does Pantoro Gold produce?

Pantoro Gold is a gold-only producer. All reported revenue and operations relate to gold extraction from Australian assets.

Where are Pantoro's mining projects located?

All of Pantoro's named projects are in Australia, with the Nicolsons Gold Mine and Norseman Gold Project both located in Western Australia. Halls Creek and a second Norseman listing are also within Australian jurisdiction.

How has PNR's share price performed over the past year?

PNR's trailing twelve-month return is flat at 0.0%, with a one-month return of -13.48%. The recent drawdown has pulled the annual return to break-even.

How does PNR's quality grade compare to its system-defined peers?

PNR holds an A+ quality grade, the top band in OreQuant's rating system. Within the five-company peer set, only Gold Reserve Inc (CVE:GRZ) shares that grade. The remaining peers are rated D, C, or F.

What does the on-market buy-back activity indicate about Pantoro?

ASX announcements show multiple buy-back notifications filed in late June 2026 followed by a cessation of securities notification in early July. This documents an active capital return program running during the period of the price decline. It is a factual corporate action data point; no directional inference about future price performance is supported by this alone.

Sources

Primary documents

- Pantoro Gold Notification of cessation of securities - PNR4 pages14.9KB · ASX · July 1, 2026 · View document

- Pantoro Gold FY2026 Result and FY2027 Guidance3 pages331.7KB · ASX · July 9, 2026 · View document

- Pantoro Gold Update - Notification of buy-back - PNR6 pages18.2KB · ASX · June 22, 2026 · View document

- Pantoro Gold Update - Notification of buy-back - PNR6 pages18.2KB · ASX · June 23, 2026 · View document

- Pantoro Gold Update - Notification of buy-back - PNR6 pages18.2KB · ASX · June 24, 2026 · View document

Risk & Disclosure

Gold mining equities carry substantial risk including commodity-price volatility, operational disruptions, jurisdictional changes, and capital allocation missteps. Senior producers mitigate some risks through diversification and scale, but remain sensitive to metal prices, cost inflation, and geopolitical developments. Junior and exploration-stage companies carry additional risk including total loss of capital. Past performance does not predict future results.

Investors should be prepared for double-digit intraday swings and should conduct independent due diligence, assess risk tolerance, and consult a licensed financial professional before initiating or modifying positions in mining equities.

OreQuant is not a registered investment advisor. This content is for informational and educational purposes only. It is not investment advice. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions. Mining equities — especially juniors — carry substantial risk including total loss of capital.

Subscribers access the full signal depth behind this snapshot — individual scores, insider cluster details, Monte Carlo valuation, and position sizing updated daily. Start Your 7-Day Free Trial.